Take control of your financial future with our process

Getting to know you

Discovery Call where I will take the time to understand your needs.

Build your mortgage plan

Create a comprehensive plan for your mortgage and a lender comparison report.

Sealed & Delivered

Sign the digital package and manage the final steps to complete your mortgage.

Future Planning

Provide ongoing support and advice for the lifetime of your mortgage.

Getting to know you

Discovery Call where I will take the time to understand your needs.

Build your mortgage plan

Create a comprehensive plan for your mortgage and a lender comparison report.

Sealed & Delivered

Sign the digital package and manage the final steps to complete your mortgage.

Future Planning

Provide ongoing support and advice for the lifetime of your mortgage.

Nice things people SAY about working with me

Specializing in the following areas

Purchase Financing

SELF-EMPLOYED

Birthday Sparks

Fashion Magazine

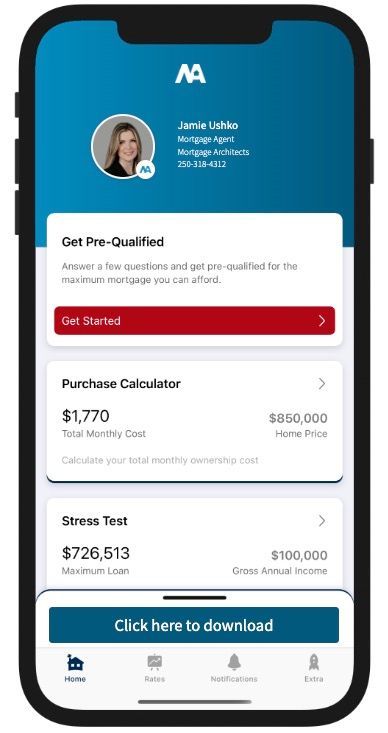

Go ahead and run some calculations.

Get started by completing my online mortgage application

I'll let you know exactly where you stand so you can proceed with confidence

Download your mortgage Planning APP

Mortgage articles to keep you informed

Go ahead and schedule a meeting with me

Covering the topics you need to become an expert in the Canadian Mortgage Industry

As an advocate for her industry, Jamie has created and produced the popular podcast "How to be a Mortgage Broker" with the goal of demystifying the startup process and helping other agents reach success quickly. This has been the perfect avenue to stay up-to-date with industry experts and branch out into new business opportunities. The best part is that all her subscribers get to follow along on the journey.